Tax surcharge on LTCG (long-term capital gain) and STCG(Short term capital gain) to FPI and domestic investors has been rolled out, i.e., they have restored the pre-budget position. An announcement was made by FM Nirmala Sitharaman on 23 August 2019 in a press conference and said India’s growth is comfortably higher than others.

The market was also keeping an eye on this conference since the market start-up early this morning. Nifty ends above 10800, Sensex gains 228 pts on stimulus hopes from FM meet.

Here are some stats of the days which will make you believe in upcoming strong market growth

Intraday Nifty chart of 23rd August 2019

The market started in the morning from Nifty at 10751 to its lowest at 10640 almost 1% down in 30 minutes span.

At the closing time, Nifty rose to 10829 so technically 2% up from the lowest number intraday. This is an observation of the market on 23 august 2019.

So Why did the Nifty jump to almost 2% high?

It was majorly a sentimental flick. The market reacted to the expectation of FM’s conference outcome of rollback of surcharge on FPIs and some other reforms to boost the economy.

Not just Nifty other Indices reacted the same Nifty Midcap 100 ended 1.18% high Nifty small cap 100 ended 0.80% high

Conclusion to the above study

The market is correcting downwards continuously and gained speed after the Union budget 2019.

Now as per today’s observation we can clearly see that a sentimental flick is taking the market upwards, investors are eagerly waiting to put money in the market after a long correction and FM gave them the reason to hit hard. India is still an attractive destination to invest in the long term despite some small factors in the short term.

Now markets will react on Monday as the conference was after the closing. Most likely expectations of investors are fulfilled we can see a good positive number on Monday.

A rise or fall in the repo rate can affect your debt repayments, savings, and investment – the volatility can even affect your ability to buy a property. We demystify the complexity behind interest and lending rates.

Here are some key insights.

Let’s start with the basics.

What is the repo rate? The repo rate, also known as the repurchase rate, is the rate at which the Reserve Bank of India lends money to the banks. The banks, in turn, lend money to their clients.

What is the repo rate?

So, how does the Reserve Bank’s repo rate affect a bank’s prime lending rate? More importantly, how does it affect you as a young person when you’re seeking a loan or opening a savings product?

Here’s how the repo rates may affect you in the short and long term.

1. Repo rates affect lending –

The Reserve Bank’s main purpose is to stabilize our currency and economy. Often a higher repo rate is used to slow inflation. Money becomes more expensive for banks to borrow, which means your credit becomes more expensive too.

2. Repo rates affect property prices –

When the repo rate rises, so do property prices. Buying a home or investment property becomes more expensive as you simply don’t have the same buying power.

To offset this, you could think about putting down a higher deposit on a new place or look at buying a more modestly priced property.

If you are willing to wait for interest rates to drop, you can possibly get more value for your money when buying property. If you are lucky enough to be a cash buyer, you can make a huge savings.

3. Repo rates affect your return on savings

The good news is that a higher repo rate, conversely, affects your savings potential. When interest rates rise, so do your returns on savings. Of course, other factors could influence savings.

Reserve Bank of India cuts repo rate by 35 basis points, EMIs to go down!

The Repo rate is the interest rate at which the Central Bank (RBI) lends money to banks. When the cost of borrowing goes down for banks, they can lower their marginal cost of funds-based lending rate (MCLR), which directly impacts loans

Since April 2016, all loans sanctioned by banks including car loans and home loans are linked to the bank’s MCLR. A lower MCLR will effectively mean a lower interest rate and, thereby, a low-interest burden, other factors remaining constant. A cut in the bank’s MCLR benefits all car loan and home loan, borrowers. “This rate cut will have a direct impact on the real estate sector, provided the banks, in turn, transmit the same by a corresponding reduction in lending rates to those seeking home loans.

The MLCR of banks has been falling but at a lesser pace. State Bank of India (SBI) had cut its MCLR by 5 basis points across all tenors with its 1-Year MCLR coming down from 8.45 percent per annum to 8.40 percent per annum with effect from 10th July 2019. In the case of Bank of Baroda, ( effective 07.07.2019 ) the 1-year MCLR is 8.60 percent. The effective home loan interest rate will be a one-year MCLR plus 1 percent based on the applicant’s risk rating. Therefore, the effective Bank of Baroda home loan interest rate will vary between 8.60 percent and 9.60 percent. For HDFC, a housing finance company, the interest rate is linked to its internal benchmark, Retail Prime Lending Rate (RPLR) on which it announced a cut of 10 basis points effective August 1, 2019.

New home loan borrowers can now start exploring home loan options with the banks. Do not merely look at the bank’s MCLR but know the actual home loan interest rate before finalizing the deal. Banks are allowed to charge a Mark-Up on the MCLR before disbursing the loan. Finally, make a pre-payment to repay the home loan as soon as possible and own your home with 100 percent equity of your own.

RBI has also trimmed the GDP growth forecast for the current fiscal to 6.9 percent from 7 percent.

If rates are higher, you should take advantage of the rise and look at putting some money away in a notice or fixed deposit savings account.

One should always plan their tax-related investments in advance and invest through the SIP route in ELSS to get the benefit of rupee cost averaging. – In simple words – “Tax saving”

By investing in ELSS mutual funds, one is eligible for tax deduction up to Rs. 1,50,000 u/s Section 80C of Income Tax Act. If you invest Rs. 1,50,000 in ELSS, you will save Rs. 45,000 (30% on the top tax bracket). So, the amount that you plan to invest in ELSS can be deducted from your income before calculating taxes. This is subject to an overall cap of Rs. 1,50,000 on the investment amount along with other tax-saving instruments

Start investment early

Many taxpayers normally tend to start investing in ELSS funds saving instruments at the end of the financial year, when the time to submit investment proof is upon them. This is a bad investment and tax-planning strategy. In such a situation, one could face cash flow-related problems towards the end of the financial year. Moreover, investing towards the end of the year forces the investors to put a lump sum amount in ELSS. This, in turn, creates the risk of market timing. If the equity markets are up, the investor ends up purchasing the fund’s units at higher valuations, which in turn affects his returns. One should always plan their tax-related investments in advance and invest through the SIP route in ELSS to get the benefit of rupee cost averaging.

Continue to invest beyond three years

Of all the tax-saving products, ELSS funds offer the shortest lock-in of three years. In other products, the lock-in period varies from 5 to 15 years. A common mistake most investors make is to redeem their investments in ELSS as soon as the three-year lock-in ends. Since the underlying asset class here is equities, they should stay invested for a time horizon of at least five-seven years to garner good returns. Hence, one should not pull out his money as soon as the three-year lock-in ends. While ELSS gives a tax break, it also has the potential to generate superior returns when compared to other asset classes as well as beat inflation in the long run. ELSS funds are the best in the tax-saving lot to date as these funds suit every category of investor.

Betting on the current best performers

The funds that are topping the charts currently (in terms of trailing returns over the past one or three years) may not be the best choice for you. Instead, investors should focus on funds that have a track record of consistency. To select a consistent fund, one must compare the fund’s performance with the average returns generated by the category year-wise for the past five or seven years. Another alternative is to compare rolling returns. This is a good measure for capturing consistency. Another commonly observed mistake is that investors put their money in a new ELSS fund every year. Over an 8–10-year period, they end up accumulating many ELSS funds. This causes excessive diversification and results in cumbersome portfolios that become hard to monitor.

Key Takeaways

Investors looking to save on tax should avoid ELSS funds if they are not comfortable with equities. ELSS is an ideal tax-saving vehicle only for those investors who are willing to stay invested for the long term, understand volatility, and are willing to ride through it. Further, one should plan these investments as early in the year as possible. If you haven’t done so, then this is the right time to plan for the next financial year in April itself. And once you start, there’s no need to stop investing next year. Since the best way to invest regularly in a fund is through SIP, you should just start one in a carefully chosen ELSS fund and let it run for a long duration.

Atal Bihari Vajpayee may have passed away but not his achievements and lessons. Long live and prosper, Atal Bharat

Key take always and achievements by Shri Atal Bihari Vajpayee, that sprung up major political, financial, development, and social reforms in Indian history:

1. Atal Ji in Numbers:

– Lived 93 years (25 Dec 1924 – 16 Aug 2018) – 10th Prime Minister of India – Prime Minister 3 times (13 days in 1996, for a period of eleven months from 1998 to 1999, and then for a full term from 1999 to 2004) – In his 3rd term as PM, the GDP rate was above 8%, inflation was below 4% and foreign exchange reserves were overflowing.

2. Look East policy:

“Look East” policy was developed and enacted during the governments of prime ministers P.V. Narasimha Rao (1991–1996) and further developed by Atal Bihari Vajpayee (1998–2004). The Look East policy back then emerged as an important foreign policy initiative of India in the post-Cold War period, following the collapse of the Soviet Union.

Lesson: Always keep good relationships with your neighbors.

3. Catapulting India on the nuclear map:

True to his name, Shri Atal Bihari Vajpayee gave the green flag to Operation Shakti (also known as the Pokhran test) and made the hero of this achievement, Dr. APJ Kalam the next President of India, who was later named the true People’s President. Vajpayee coined the slogan: ‘Jai Jawan, Jai Kisan, Jai Vigyan’. He promoted the scientific spirit, and not just technology.

Lesson: Embracing science & Use of technology, will lead to a safer, better, and brighter future

Quote by PM Shri Atal Bihari Vajpayee: “Our nuclear weapons are meant purely as a deterrent against nuclear adventure by an adversary.”

And thus, India made its foothold in the regional and global political scenario. Even after sanctions were imposed by western countries, India grew at a constant rate. This will lead to the first-ever US presidential visit to India.

Lesson: Never get fazed by the competition (even if they are bigger than you are) and keep moving forward.

4. Kargil War:

When Militants and Pakistani soldiers infiltrated across the Line of Control (LoC) in J&K & captured hilltops, and unmanned border posts, Shri Atal Bihari Vajpayee said, “we will get them out, one way or the other”.

Lesson:A leader never backs down even if a win comes at a cost.

5. National Highway Development Project (NHDP)

To construct world-class highways in India, connecting the four major cities of Delhi, Mumbai, Chennai, and Kolkata (‘Golden Quadrilateral’) & Pradhan Mantri Gram Sadak Yojana Connecting all four major cities and villages in India was an unprecedented move from the Prime Minister’s office. Shri Atal Bihari Vajpayee’s vision played a very important role in improving logistics on a national scale. All big e–com giants like Flipkart, Snapdeal, Amazon, etc. may be selling goods online but are getting delivered at your doorsteps (faster than ever) using the same highways.

Lesson:Connecting people always pay a rich dividend in the long term

6. First UN speech in Hindi

Shri Atal Bihari Vajpayee gave a speech in Hindi at the 1977 UN General Assembly Speech as India’s Foreign Minister in the Janata Party Government. That was the first time anyone had given a speech in Hindi at the global forum.

Lesson:Believing in your skills and don’t be shy to present it.

7. Leading the first successful coalition government

“India Has to Run On Consensus” said Shri Atal Bihari Vajpayee (To watch full NDTV interview: click here).

Lesson: a. Always listen to your audience, always. b. Even if it is hard to manage but nevertheless, Team is better than going solo.

8. Setup of Disinvestment Ministry

Now Known as Department of Investment and Public Asset Management the Department of Disinvestment was set up as a separate Department on 10th December, 1999 and was later renamed as Ministry of Disinvestment form 6th September, 2001. These are some important mandates:

All matters relating to management of Central Government investments in equity including disinvestment of equity in Central Public Sector Undertakings.

All matters relating to sale of Central Government equity through offer for sale or private placement or any other mode in the erstwhile Central Public Sector Undertakings

Decisions on the recommendations of Administrative Ministries, NITI Aayog, etc. for disinvestment including strategic disinvestment

All matters related to Independent External Monitor(s) for disinvestment and public asset management.

Lesson: There should always be an oversight or a consultant in all matters related to investment(s).

9. Telecom revolution with new telecom policy:

In 1999, Vajpayee government took a decision to end state monopolies for entities like Bharat Sanchar Nigam Limited (BSNL) and introduced a new Telecom Policy which led to revenue sharing model and eventually paved the way for call rates getting cheaper as well as affordable mobile phones.

Lesson:Sharing is a call for all.

10. Introduced Education as fundamental right

Under Vajpayee government a mission named “Sarva Shiksha Abhiyan” was started. The mission was to provide free and compulsory education to all children between 6 and 14 years of age. The primary objective of the scheme, which commenced in 2000-01, was to reduce dropouts and increase the net enrolment ratio at primary level. In fact, the song School Chale Hum that was used to promote the scheme was penned by Vajpayee himself. With the mission in full force, the rate of dropouts reduced from almost 40 percent in 2000 to less than 10 percent in 2005.

Lesson: Education leads to the betterment of oneself, the society, and the nation.

11. Flags off IIndia’s first modern rail project (Delhi metro)

Former Prime Minister Atal Bihari Vajpayee had gifted the very first Delhi Metro to the national capital. Vajpayee in 2002 inaugurated the Delhi Metro, fulfilling a long-cherished dream of an underground rail. “Hamare liye garv ki baat hai ki 24 December 2002 ko Atal Bihari Vajpayee iss desh ke sabse pehle metro ke passenger bane they” said current PM Narendra Modi on December 25 to launch the Magenta line of the Delhi metro.

Lesson: Technology and infrastructure are two wheels on a non-stopping development train.

Public Provident Fund (PPF) scheme is a popular long-term investment option backed by the Government of India which offers safety with returns that are fully exempted from Tax. Investors can invest a minimum of Rs. 500 to a maximum of Rs. 1,50,000 in one financial year and can get the facilities such as loan, withdrawal, and extension of account. Also, the total lock-in for the PPF account is 15 years which is too high compared to other instruments available like Mutual fund ELSS, NSC, etc.

Features of PPF account

The interest rate of 8% per annum.

Minimum and maximum investment Rs.500 & 1.5L per annum.

The Lock-in period is 15 Years.

Partial withdrawal is available after 7 years.

After 15 years account can be extended for a block of 5 years.

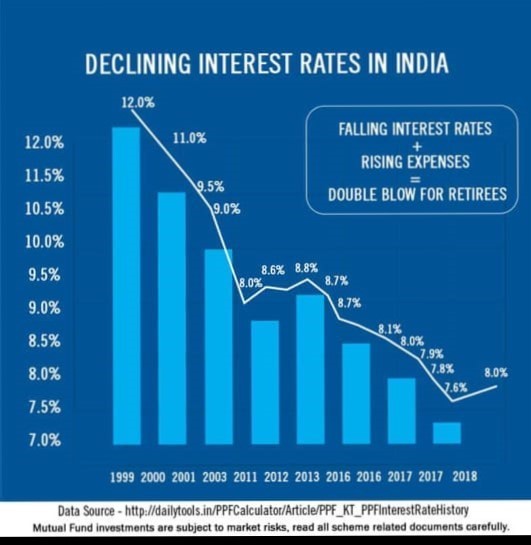

PPF has become less attractive over a period since it started declining interest rates, have a look

Declining rates of PPF

Rates were fixed at 12% between 1986 and 2000

Then between 2000 and 2003, the rates slid down to 8%

The rates then remained stable at 8% till 2011

Rates were then revised to 8.6%, 8.8%, and 8.7%.

The last few years saw rates come down to 8.1%, 8.0%, 7.9%, 7.8%, and then a historic low of 7.6%.

Rates finally saw an uptick of 8.0%.

With effect from 1st April 2016, the rates for schemes like PPF, etc. are to be considered for revision every quarter, based on the previous quarter’s yield on benchmark government securities (or bonds of corresponding maturities) with a small markup (around 0.25%).

What’s the risk?

Earlier, rates were revised once every year. But now, the revision will take place every quarter.

So, there is obviously an increase in interest rate risk as far as PPF is concerned. So, in a falling rate scenario and for someone who has a large PPF balance, it can hurt a lot.

Also, Lock-in for PPF is 15 years and in 15 years we have 60 quarters for rate fluctuation which is high.

Now, what to do?

You can check for various alternatives like NSC, ELSS (mutual funds), Tax saving bonds, etc. But among tax-saving instruments, the clear winner as of now is ELSS (Mutual fund) but a subsequent risk is also involved with it.

The risk-reward ratio works with mutual funds the higher the risk you take the more returns you get. Also, the ELSS Mutual fund has the lowest lock-in period of just 3 years. The average return in ELSS Schemes for the last 5 years is 12-16% per annum which is much higher than PPF, NSC Fixed deposits, etc.

Now let’s choose the best option with comparison.

ELSS VS PPF VS FIXED DEPOSITS

Particulars

ELSS (Mutual funds)

PPF

Fixed deposits

Objective

Growth with Income tax rebate under sec 80C

Limited growth with Income tax rebate under sec 80C

Limited growth with Income tax rebate under sec 80C

Lock-In period

3 years

15 years

5 years

Average Return

12-16%*

7-9%

7-8%

Risk

Moderate to High

Low

Moderate

Maturity

After 3 years but can be kept for appreciation to n number of years

After 15 years but can be extended in block of 5 years.

After 5 years and cannot be extended

Tax

10% LTCG on returns if gains are higher than1 lac

No tax

Taxable as per Income tax slab.

Post-tax Return

10.8 – 14.4%**

7-9%

5.6 – 6.4%***

*Returns are subject to market conditions; returns are indicated as per past performance and can be changed in the future.

** After deducting 10% LTCG from average returns.

*** After deducting tax rated as 20% tax bracket.

Conclusion

PPF is no more an attractive option for tax savings rather If you can take moderate to high risk then you can opt for ELSS Mutual funds. Each investment is associated with certain positive and negative Parameters (mentioned in the above table).